Register now or log in to join your professional community.

The accounts payable process or function is immensely important since it involves nearly all of a company's payments outside of payroll. The accounts payable process might be carried out by an accounts payable department in a large corporation, by a small staff in a medium-sized company, or by a bookkeeper or perhaps the owner in a small business.

Regardless of the company's size, the mission of accounts payable is to pay only the company's bills and invoices that are legitimate and accurate. This means that before a vendor's invoice is entered into the accounting records and scheduled for payment, the invoice must reflect:

To safeguard a company's cash and other assets, the accounts payable process should have internal controls. A few reasons for internal controls are to:

Periodically companies should seek professional assistance to improve its internal controls.

The accounts payable process must also be efficient and accurate in order for the company's financial statements to be accurate and complete. Because of double-entry accounting an omission of a vendor invoice will actually cause two accounts to report incorrect amounts. For example, if a repair expense is not recorded in a timely manner:

If the vendor invoice for a repair is recorded twice, there will be two problems as well:

In other words, without the accounts payable process being up-to-date and well run, the company's management and other users of the financial statements will be receiving inaccurate feedback on the company's performance and financial position.

A poorly run accounts payable process can also mean missing a discount for paying some bills early. If vendor invoices are not paid when they become due, supplier relationships could be strained. This may lead to some vendors demanding cash on delivery. If that were to occur it could have extreme consequences for a cash-strapped company.

Just as delays in paying bills can cause problems, so could paying bills too soon. If vendor invoices are paid earlier than necessary, there may not be cash available to pay some other bills by their due dates.

A purchase order or PO is prepared by a company to communicate and document precisely what the company is ordering from a vendor. The paper version of a purchase order is a multi-copy form with copies distributed to several people. The people or departments receiving a copy of the PO include:

The purchase order will indicate a PO number, date prepared, company name, vendor name, name and phone number of a contact person, a description of the items being purchased, the quantity, unit prices, shipping method, date needed, and other pertinent information.

One copy of the purchase order will be used in the three-way match, which we will discuss later.

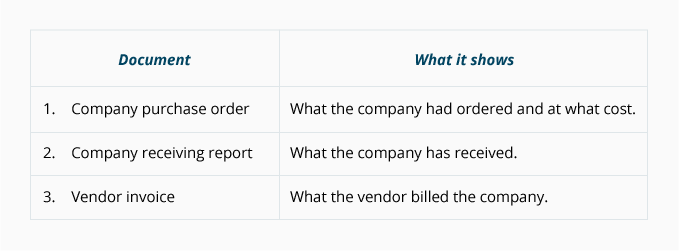

A receiving report is a company's documentation of the goods it has received. The receiving report may be a paper form or it may be a computer entry. The quantity and description of the goods shown on the receiving report should be compared to the information on the company's purchase order.

After the receiving report and purchase order information are reconciled, they need to be compared to the vendor invoice. Hence, the receiving report is the second of the three documents in the three-way match (which will be discussed shortly).

The supplier or vendor will send an invoice to the company that had received the goods and/or services on credit. When the invoice or bill is received, the customer will refer to it as a vendor invoice. Each vendor invoice is routed to accounts payable for processing. After the invoice is verified and approved, the amount will be credited to the company's Accounts Payable account and will also be debited to another account (often as an expense or asset).

A common technique for verifying a vendor invoice is the three-way match.

The accounts payable process often uses a technique known as the three-way match to assure that only valid and accurate vendor invoices are recorded and paid. The three-way match involves the following:

Only when the details in the three documents are in agreement will a vendor's invoice be entered into the Accounts Payable account and scheduled for payment.

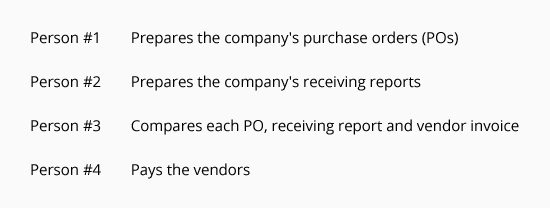

Good internal control of a company's resources is enhanced when the company assigns a separate employee with a specific, limited responsibility. The following chart illustrates the concept of the separation (or segregation) of duties involving accounts payable:

When the duties are separated, it will require more than one dishonest person to steal from the company. Hence, small companies without sufficient staff to separate employees' responsibilities will have a greater risk of theft.

To illustrate the three-way match, let's assume that BuyerCo needs 10 cartridges of toner for its printers. BuyerCo issues a purchase order to SupplierCorp for 10 cartridges at $60 per cartridge that are to be delivered in 10 days. One copy of the PO is sent to SupplierCorp, one copy goes to the person requisitioning the cartridges, one copy goes to the receiving department, one copy goes to accounts payable, and one copy is retained by the person preparing the PO. When BuyerCo receives the cartridges, a receiving report is prepared.

The three-way match involves comparing the following information:

After determining that the information reconciles, the vendor invoice can be entered into the liability account Accounts Payable. The information entered into the accounting software will include invoice reference information (vendor name or code, invoice number and date, etc.), the amount to be credited to Accounts Payable, the amount(s) and account(s) to be debited and the date that the payment is to be made. The payment date is based on the terms shown on the invoice and the company's policy for making payments.

Lastly, the documents should be stamped or perforated to indicate they have been entered into the accounting system thus avoiding a duplicate payment.

Some companies use a voucher in order to document or "vouch for" the completeness of the approval process. You can visualize a voucher as a cover sheet for attaching the supporting documents (purchase order, receiving report, vendor's invoice, etc.) and for noting the approvals, account numbers, and other information for each vendor invoice or bill.

When the vendor invoice is paid, the voucher and its attachments (including a copy of the check that was issued) will be stored in a paid voucher/invoice file. If paper documents are involved, an office machine could perforate the word "PAID" through the voucher and its attachments. This is done to assure that a duplicate payment will not occur.

The unpaid invoices and vouchers will be held in an open file.

Not all vendor invoices will have purchase orders or receiving reports. Hence, the three-way match is not always possible. For example, a company does not issue a purchase order to its electric utility for a pre-established amount of electricity for the following month. The same is true for the telephone, natural gas, sewer and water, freight-in, and so on.

There are also payments that are required every month in order to fulfill lease agreements or other contracts. Examples include the monthly rent for a storage facility, office rent, automobile payments, equipment leases, maintenance agreements, etc. Even though these obligations will not have purchase orders, the responsibility is unchanged: pay only the amounts that are legitimate and accurate.

Vendors often send statements to their customers to indicate the amounts (listed by invoice number) that remain unpaid. When a vendor statement is received the details on the statement should be compared to the company's records.

The fact that a company can be receiving both invoices and statements from a vendor means there is the potential of a duplicate payment. In order to avoid making a duplicate payment, companies often establish the following rule: Pay only from vendor invoices; never pay from vendor statements.

Purchase Invoice, Vendor Invoice, Note Payable, Payment on Delivery, Installment Payable slip,

The mission of accounts payable is to pay only the company's bills and invoices that are legitimate and accurate.

The accounts payable process often uses a technique known as the three-way match to assure that only valid and accurate vendor invoices are recorded and paid. The three-way match involves the following and this are the documents need to be reviewed before making the payment.

1. Company Purchase Order

2. Company Receiving Report

3. Vendor Invoice

First of all checked out Purchase order reference number, after than verify the supplier invoice detail such as rate, qty taxes are matched with the PO, GRN, Delivery note and material satisfaction note, magement approvels and crediy time period after check all things done u should clear the payment. Thanks....

Following documents needed while payment to supplier.

1-Quotation

2-invoice from supplier (compulsory)

2-delivery note as well

3- Receipt after payment

Vendor Invoice, PO, PV, Devivery Note-Quatation or Offer also can be refered

Supplier's Invoice, Purchase Order, GRN/MRN, Delivery Note, Payment Voucher etc.

More or less following documents might be required

1.. copy of Signed contract or Purchase order it is depend on the volume of transactions

2... Goods Received Note

3.. Inspection Report/Technical report

4... lab testing report (in some cases like food, medicines etc)

5... Original Invoice

6... Approval as authority matrix of your organization

7... Availability of approved budget

8...Project completion report in case of consultants/construction projects

First, upon receipt of goods you need to match the purchase order with the delivery note and invoice and ensure no discrepancies occur, and ensure that the inventories/asset received are in good hand. Then a good receipt note should be prepared and recorded in the system. Then based on the agreed credit period (could be from 0-90 days) the supplier is entitled to receive their payment. Once cheque is issued proper review and approval by management depending on the amount.

Goods received note to be reviewed whether we received goods as per purchase order or not

Then invoice quantity should be tally with the goods received note quantity

off set the debit note if any.